Malaysia Petroleum Management

-

Introduction

The Shallow Water Enhanced Profitability Terms (EPT) Production Sharing Contract (PSC) is simpler yet reflects a progressive and innovative approach to adapt to the prevailing business environment. It is tailored to match the hydrocarbon opportunities that lies in Malaysia shallow water blocks.

The EPT will replace the 1997 Standard Revenue Over Cost (R/C) PSC Terms for future shallow water exploration contracts. Through this major shift, PETRONAS aspires to create new positive “experiences” among investors in creating opportunity to maximise value from their investments and dealing with PETRONAS as a customer focused host authority. Our objective is to provide investors with flexible, competitive and progressive terms.

In designing the EPT, PETRONAS took into consideration the industry challenges and investors’ feedbacks gathered from various bid round platforms, negotiations and engagements.

Given the changing business landscape in this new decade and the current low oil price scenario, the enhancement is timely to facilitate investors in securing investment funds that meet their overall corporate strategic plans and hurdle rates.

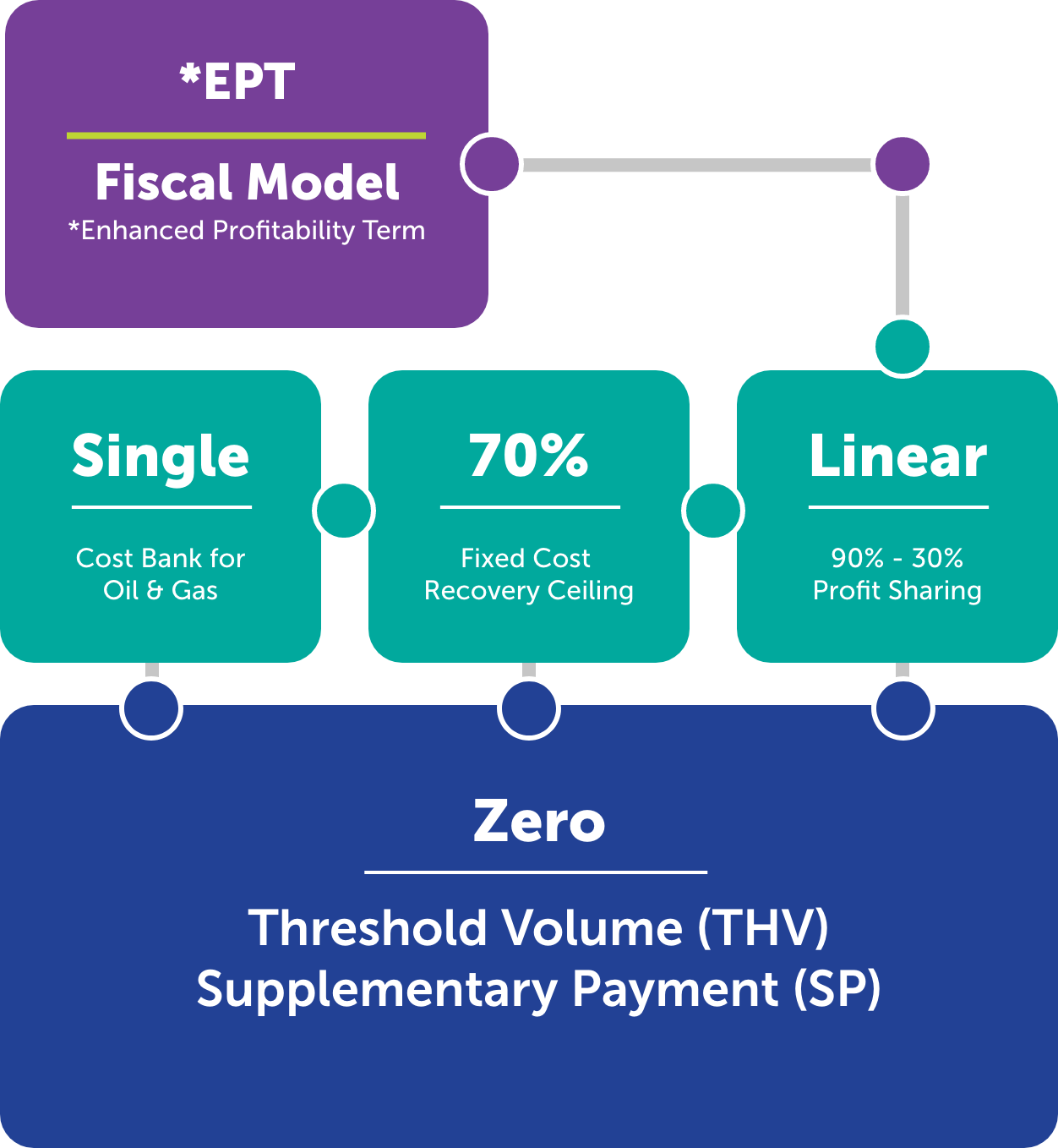

The EPT comprises a single cost bank for oil and gas, a fixed cost recovery ceiling and a more responsive self-adjusted profit-sharing mechanism. It removes the Supplementary Payment (SP) and Threshold Volume (THV) provisions to provide a more equitable sharing of upside rewards. With these improvements, EPT offers a more attractive returns to the PSC contractors that commensurate with the level of risk exposure.

Illustration on the Fiscal Model

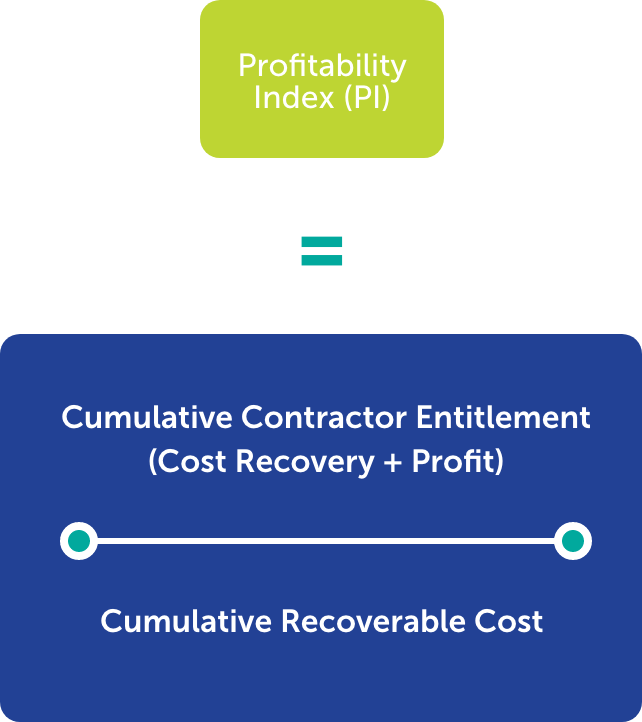

Profitability Index (PI)

Cost Ceiling

Contractor Profit Share

0.0 ≤ PI ≤ 1.5

70%

90%

1.5 < PI ≤ 2.5

Interpolation

PI > 2.5

30%

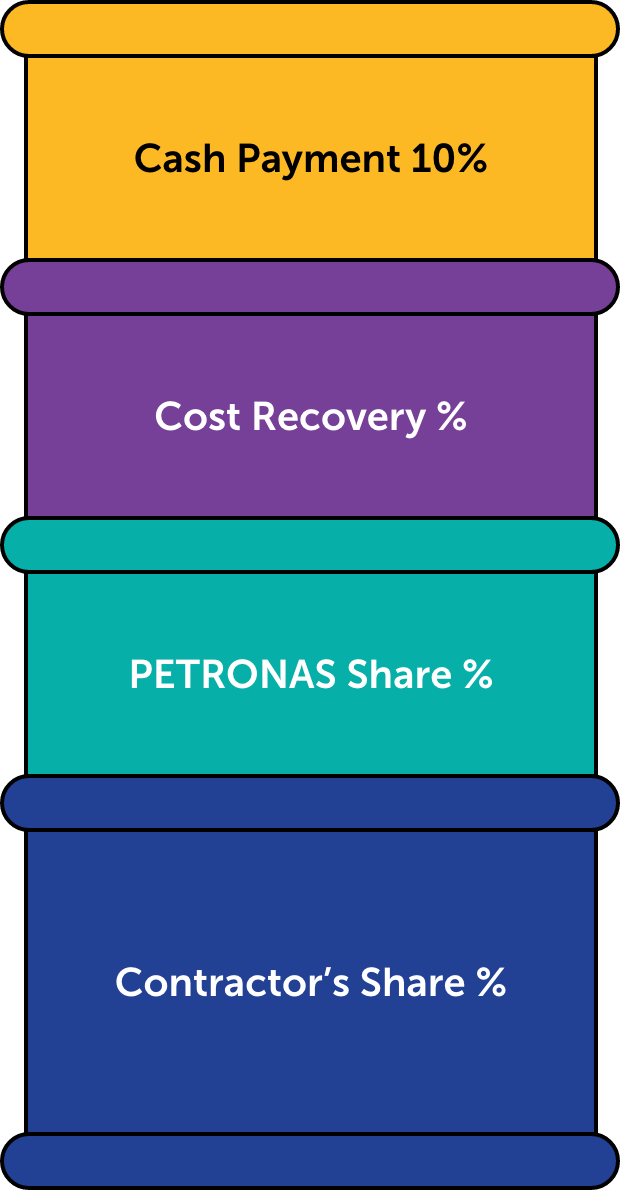

Revenue Distribution

Under the EPT, cost recovery and profit sharing are based on a single oil and gas pool instead of separate accounts of oil and gas to simplify PSC management.

Cash Payment

Cash payment to the Federal and State Governments is 10 per cent of the gross production.

Cost Recovery Ceiling

The cost recovery ceiling is fixed at 70 per cent of the gross production to accelerate cost recovery and provide a more stable recovery pool throughout the life of the PSC.

Profit Sharing

The remaining production after cash payment and cost recovery is treated as profit that is shared between PETRONAS and contractor based on the self-adjusted profit-sharing mechanism. Contractor’s profit share is tied to the profitability index (PI) with a maximum share of 90 per cent for PI up to 1.50 and a minimum share of 30 per cent for PI equal to or more than 2.50. The interpolated contractor share between PI of 1.50 and PI of 2.50 shall be determined based on the following formula:

Contractor Profit Share = 1.8 – 0.6 x PI

The PI is represented by the cumulative contractor’s entitlement comprising the cost recovery and profit share divided by the cumulative recoverable cost from the inception.

The front loading of cash flow represented by the 70 per cent maximum cost recovery and the 90 per cent contractor profit share for profitability index up to 1.50 would accelerates the after-tax discounted payback period. In addition, the progressive adjustment provides a better buffer for contractor to manage risk under unfavourable scenarios such as lower actual price and volume downsides.

THV and SP

The THV and SP provisions are not applicable under EPT.The concept behind the EPT is to have the PI as a single value balancing mechanism for determining the profit sharing between PETRONAS and contractor that allows a more equitable sharing of upside rewards, drives reinvestments within asset and promotes multiple field developments throughout the life of the PSC.

The Non-fiscal Enhancement

Another element of risk reward investment decision equation is the exploration exposure. PETRONAS has made another step change related to this investment driver to enhance competitiveness of our Malaysia bid round through the removal of PETRONAS Carigali Sdn Bhd (PCSB) carried interest requirement.

The removal of PCSB carried interest is an effort to handle the contractor’s exploration risk exposure as well as providing capital which could be utilised to fund other exploration activities. The removal of carried interest is applicable for all future exploration PSCs in shallow water and deep water blocks.

The new enhanced shallow water EPT is designed to renew interest and investment in exploration and development of Malaysia hydrocarbon resources and will benefit contractor in many ways.

The EPT promotes fresh fiscal experiences reflected by leaner, simpler and more attractive terms to match the opportunities in our shallow water blocks. The framework is crafted for a simpler take on the overall representation of the hydrocarbon sharing arrangement. The PSC entitlement calculation will be less tedious and reduce the need for a bigger PSC administrative function.

The fiscal structure and rates are more robust for contractor to mitigate risk and uncertainty in the exploration and development of the resources and provides more equitable sharing on the upside scenarios. The EPT offers an attractive fiscal terms package to maximise value from investment, by improving contractor’s base value, providing a more equitable sharing of upside rewards and promoting reinvestments within the assets or PSC.

Our aspiration is to encourage long term investment by the investors hence supporting the efforts to sustain Malaysia’s production.

Know more about PETRONAS