Malaysia Petroleum Management

-

Late Life Assets (LLA) PSC Terms

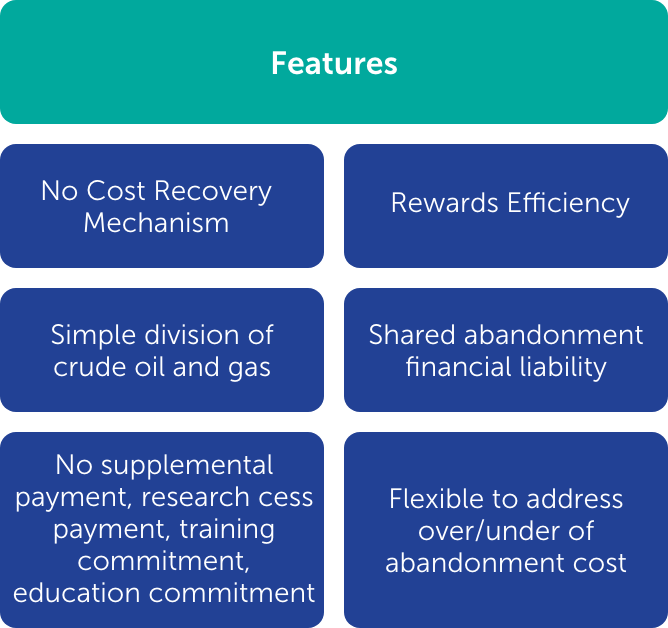

The Late Life Asset (LLA) commercial arrangement is a simplified commercial arrangement designed to empower contractors and reward efficiency with shared abandonment liability. The arrangement has no cost recovery mechanism, no supplemental payment, no research cess, no training commitment and no education commitment. The LLA arrangement rewards efficiency by encouraging cost savings and supported by simplified processes.

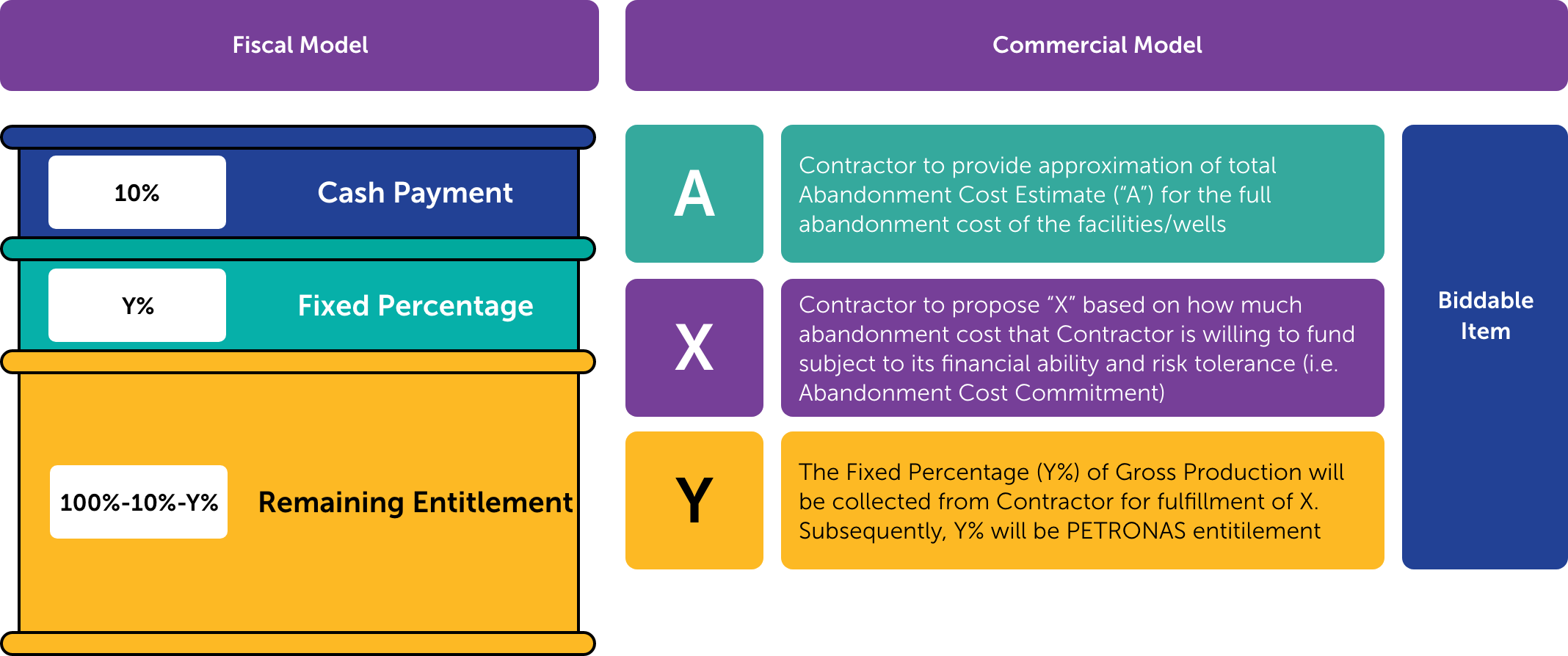

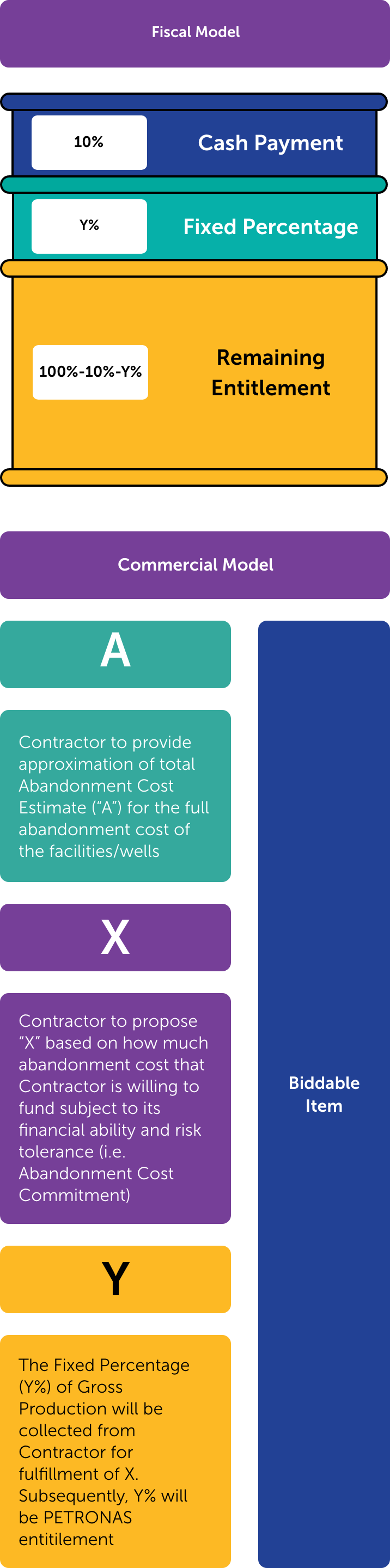

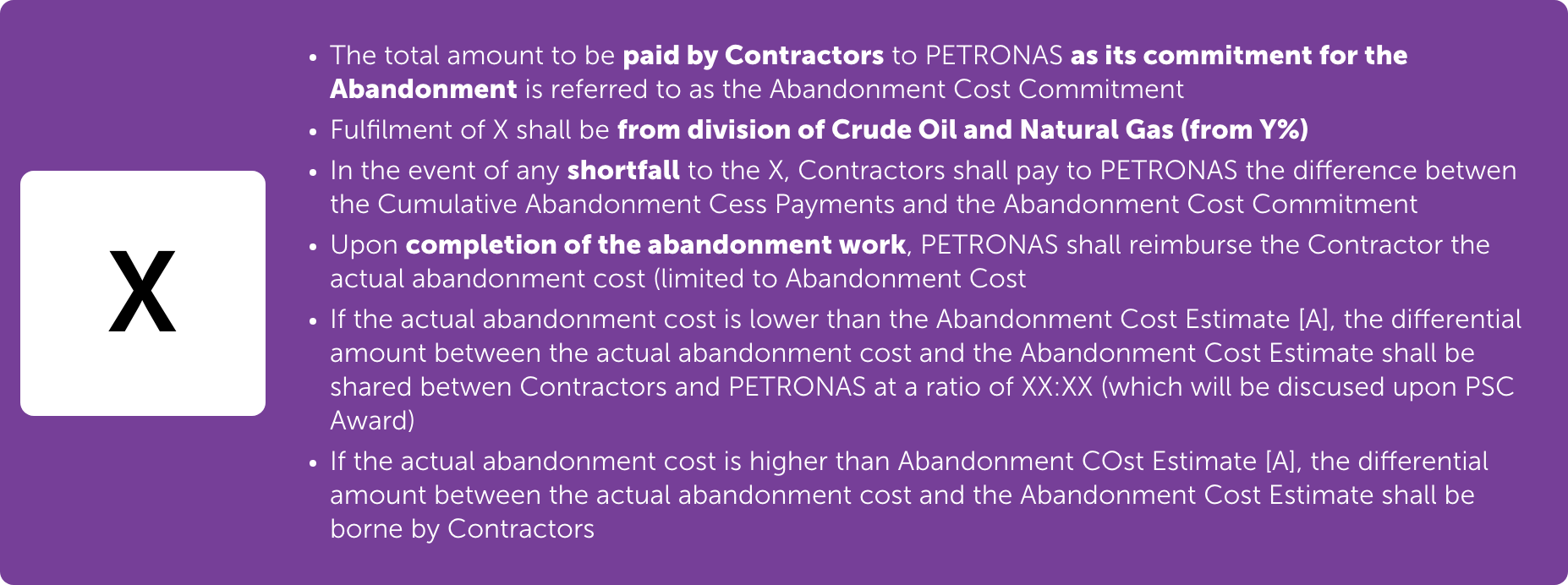

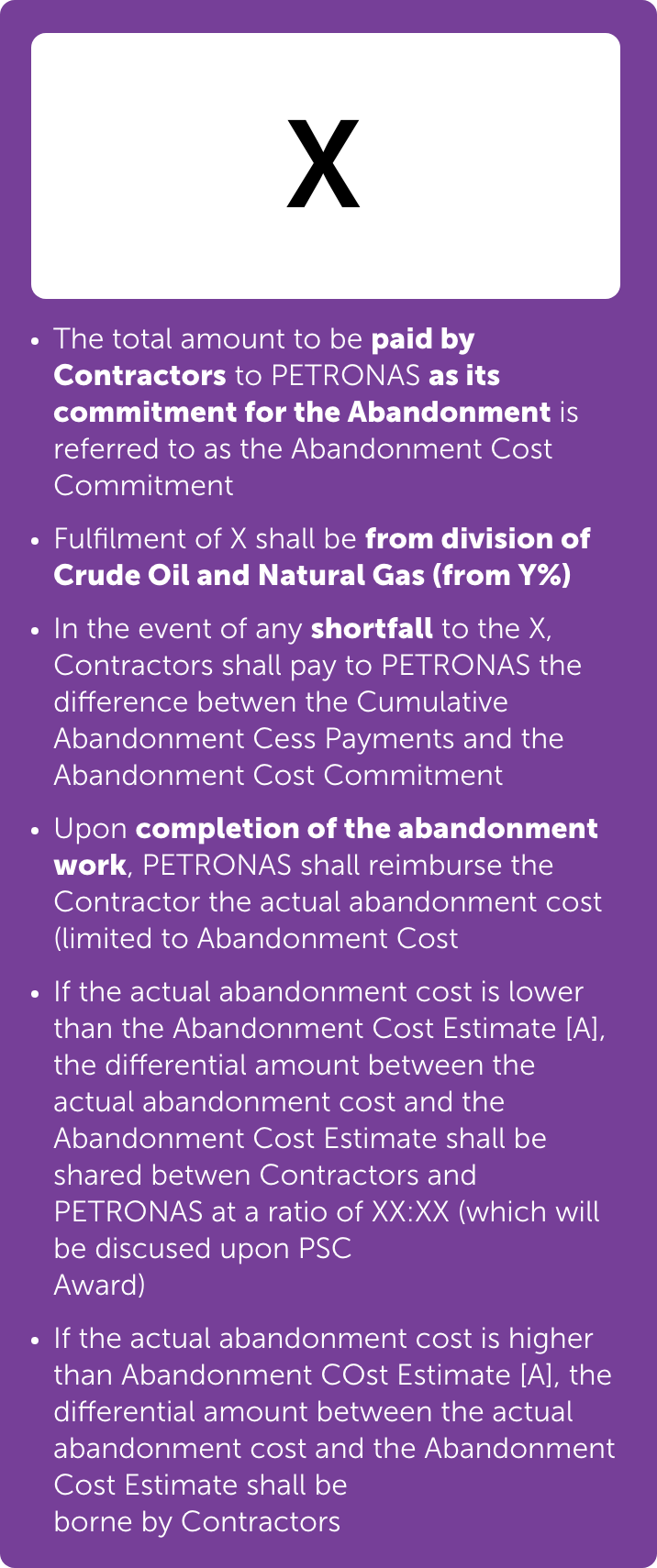

The entitlement split will be based on simple gross production division which consists of 10% cash payment to the Government and a fixed Y% of gross production to fulfill Abandonment Cost Commitment (“X”) whereas remaining entitlement shall be Contractor’s Take (100% - 10% - Y%).

There are three (3) key biddable items under this commercial arrangement, which are:

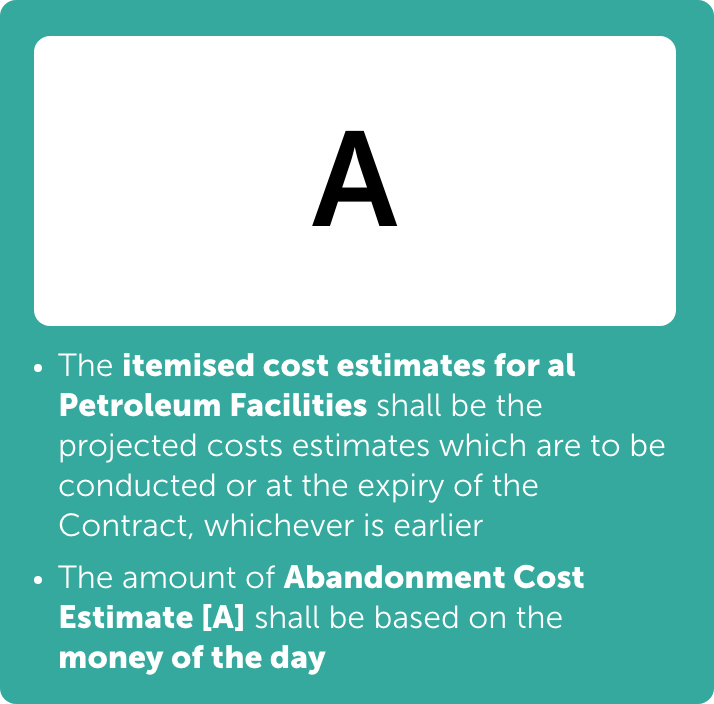

- Total Abandonment Cost Estimate (“A”);

- Abandonment Cost Commitment (“X”); and

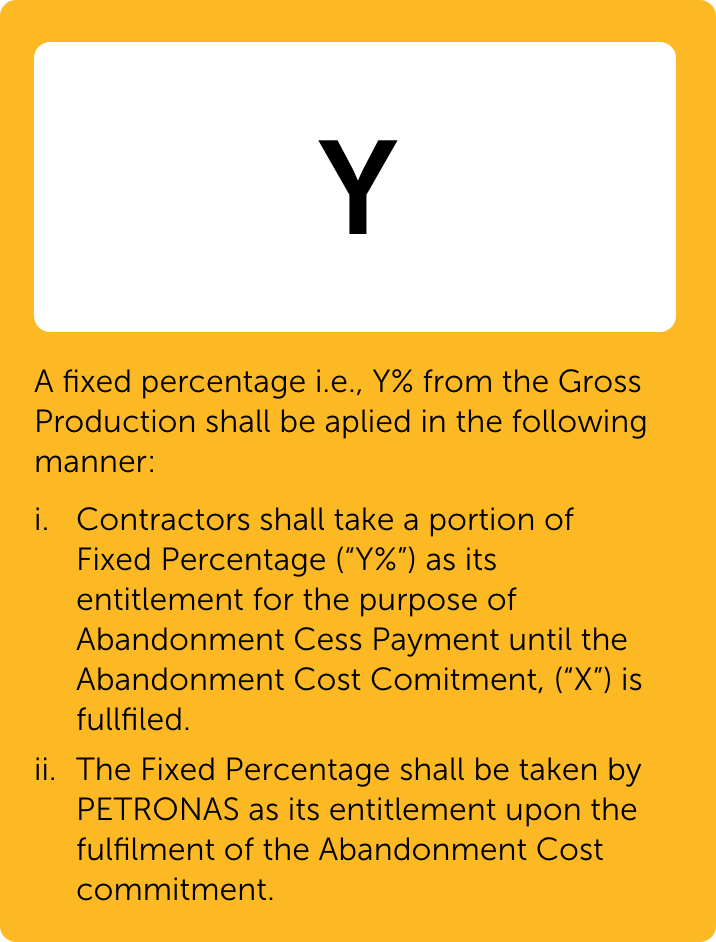

- The Fixed Percentage (Y%) of gross production.

Illustration on the Fiscal Model

I. Cash Payment

A maximum of 10% shall be taken by PETRONAS to settle cash payments to Government pursuant the Petroleum Development Act, 1974.II. Fixed Percentage (Y%)

A fixed percentage i.e., Y% from the Gross Production shall be applied in the following manner:- Contractors shall take a portion of Fixed Percentage (“Y%”) as its entitlement for the purpose of Abandonment Cess Payment until the Abandonment Cost Commitment, (“X”) is fulfilled.

- Upon fulfilment of the Abandonment Cost Commitment, the Fixed Percentage shall be taken by PETRONAS as part of its entitlement.

III. Remaining Entitlement

Remaining portion shall be taken by the Contractors (Contractor’s Take) and shall cover all costs incurred by Contractors for petroleum operations, including all tax payable under the Petroleum Income Tax Act (PITA) and Export Duty (if applicable) based on Customs Regulation. The Contractors shall pay at their own expense all Taxes, whether imposed by the Federal or State Governments or local authorities, for which Contractors are liable under the laws of Malaysia.Illustration on the Commercial Model

Based on the Fiscal Model, Contractors are to submit the bid with the following biddable parameters:

Abandonment Cost Estimate, A (USD Mil)

Abandonment Cost Commitment, X (USD Mil)

Fixed Percentage, Y (%)

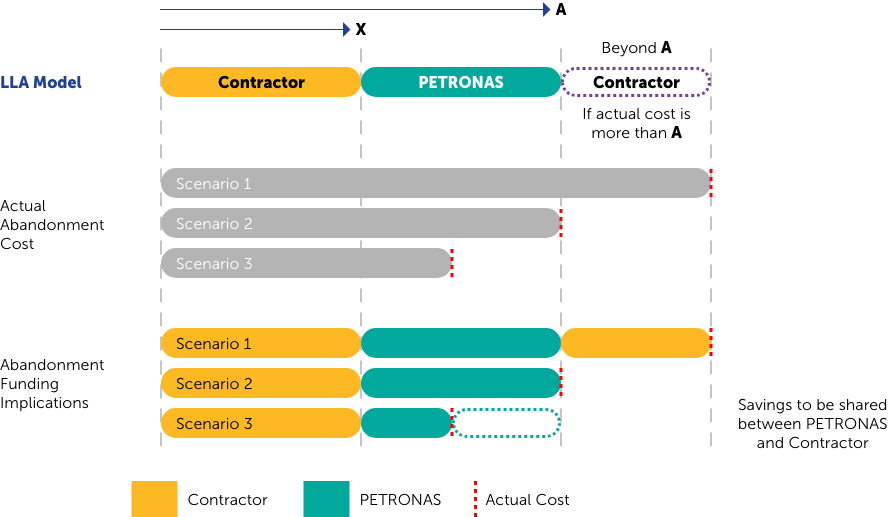

The LLA arrangement will encourage Contractors to incorporate cost saving in executing the actual abandonment activities

The above figure illustrates three (3) possible scenarios for the treatment based on the actual abandonment cost.

Scenario 1 is when the actual abandonment cost exceeds the pledged Total Abandonment Cost Estimate (“A”). In this case, the Contractor is obliged to fund the difference between the actual abandonment cost and the total Abandonment Cost Estimate (“A”).

Scenario 2 is the ideal scenario where the actual abandonment cost equals the total Abandonment Cost Estimate (“A”). In this case, the difference between the actual abandonment cost and the actual Abandonment Cost Commitment collected will be funded by PETRONAS.

Scenario 3 is when the actual abandonment cost is less than the total Abandonment Cost Estimate (“A”). PETRONAS will fund the difference between the actual abandonment cost and the Abandonment Cost Commitment (“X”).The cost saving namely the difference between the total Abandonment Cost Estimate (“A”) and the actual abandonment cost will be shared between PETRONAS and Contractor.

Sample illustration on division of production and impact to abandonment cost (based on assumptions)

Item

Bbls / year

Production (2,00 bbls/d)

730,000

Less Cash Payment (10%)

73,000

Revenue minus Cash Payment

657,000

5% Cess Contribution up to RM 10 million

36,500

85% Contractors Take (gross)

620,500

Assumptions:

- For simplicity, assume production is straight line at 2,000 bbl/d and price remains USD50/bbl.

- Production is assumed for a total of 5 years. By end of Year 5, abandonment activities needs to be undertaken by contractor.

Based on the assumptions, at the end of Year 5, Contractor needs to undertake USD100 million abandonment works for facilities and wells. USD10 million would come from the cess contribution and the remaining USD90 million will be contributed by PETRONAS.

Should the actual abandonment work be lesser than USD100 million, the difference will be shared amongst Contractor and PETRONAS.

However, should the abandonment work be more than USD100 million, the difference will be borne by Contractor. This is to incentivise Contractor to reduce costs when performing the actual abandonment activities.

Based on the illustration, a total amount of USD9.1 million would be available in the cess fund (36.5kbbls x USD50 x 5 years). Contractor will need to pay for the remaining balance of USD0.9 million (USD 10 million less USD9.1 million).

Based on the assumptions, Contractor would be able to take ~USD155 million (gross) for five years (620.5kbbls x USD50 x 5 years). Contractor is encouraged to reduce their operational and other costs to ensure a higher net take.

What‘s in it for the Contractor?

- Administratively simpler – Simplified non cost recovery fiscal model

- Contractors are incentivized to prolong the economic limit of the asset through prudent cost management

- The more production, the more Contractors will earn

- Every cent of cost saved, is a cent earned

Contact Us For Any Enquiries

Know more about PETRONAS